To introduce the subject matter related to international operations, also called Cross-Border Operations, it is necessary to individualize certain concepts that are relevant to understand the movements of the international market.

In this regard, it should be noted that "remittances", as defined in the 1946 Annual Affidavit on operations in Chile, are a way of fulfilling an obligation contracted with a person without residence in Chile, by means of the payment, distribution, withdrawal, remittance, making available or crediting in account the corresponding income.

Along the same lines, "investments abroad", which are reported by taxpayers in the 1929 Annual Affidavit on operations abroad, are mainly defined as investments in any type of assets, rights, or participations, among others, that are located abroad, likely to generate income or profits that increase the investor's equity.

Thus, in accordance with these concepts, we can point out that in the last 6 years, these international operations, whether remittances or investments, have maintained an upward trend at a general level.

In the first instance, we can show that there is an annual increase in remittances leaving Chile abroad from the 2018 business year to the 2023 business year from $17.7 to $33.5 billion5 Chilean pesos respectively, a figure that represents 11.88% of the GDP of the year 2023.

|

Remittance |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

|---|---|---|---|---|---|---|

|

GDP (1)(2) |

189,4 |

195,8 |

200,3 |

240,6 |

262,6 |

281,9 |

|

Remittance (1) |

17,7 |

19,2 |

20,1 |

30,9 |

30,6 |

33,5 |

|

Percentage |

9,30% |

9,80% |

10,00% |

12,80% |

11,70% |

11,88% |

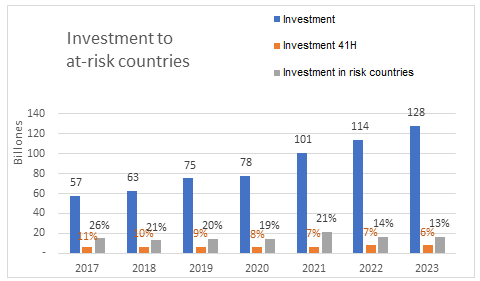

In the same way, there is also an increase in the accumulated number of investments that Chileans make abroad, with a figure of $62.8 billion Chilean pesos in 2018 and $127.6 billion Chilean pesos in 2023, equivalent to 45.30% of GDP.

|

Investments |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

|---|---|---|---|---|---|---|

|

GDP (1)(2) |

189,4 |

195,8 |

200,3 |

240,6 |

262,6 |

281,9 |

|

Investment (1) |

62,8 |

75 |

77,50 |

100,8 |

113,4 |

127,6 |

|

Percentage |

33,10% |

38,30% |

38,70% |

41,90% |

41,90% |

45,30% |

In this same context, it should be noted that the main countries that receive remitted income from Chile, until the 2023 business year, are the United States of America, the United Kingdom, Spain, Canada, and Japan (57.6% of total remittances for that year).

Return on Chilean Investments Abroad

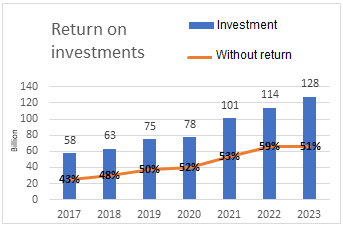

With respect to Chilean investments abroad, although there is an increase in the number of investments in the indicated periods (2017 to 2023), the income associated with such investments (profitability) has been maintained in the last years analyzed (2022 and 2023), in general terms.

It should be noted that the percentage of investments without profitability, that is, that do not generate taxable income in Chile during a business year, maintained its increase until 2022, a situation that could be due to:

- New investments in the corresponding year.

- Legitimate business reasons, such as the implementation of market penetration strategies or others that hope to generate profitability in the future.

- They could directly be situations of tax evasion or avoidance.

However, for this last year under analysis, there is a slight decrease in

these investments without return.

The SII's strategy has incorporated periodic monitoring of international indicators or

metrics that

not only account for the behavior of taxpayers in terms of economic indicators,

but also allows observing the use of exemptions from the Income Tax Law, to

evaluate that they are used appropriately and ensure that they are not exploited

to gain an advantage not foreseen by the legislator. In the analysis of these

metrics, both the movement of investments and the movement of remittances

abroad are visualized, allowing a broad vision of the international scenario

that this country faces

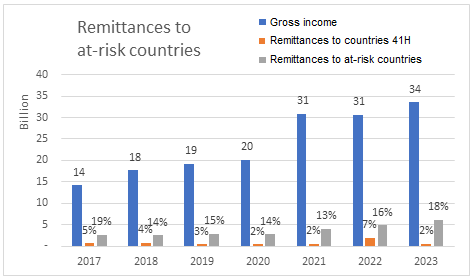

Remittances abroad

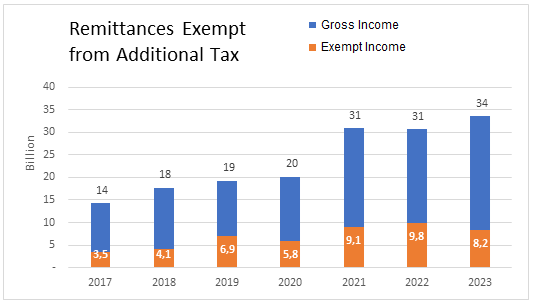

Tax-exempt remittances abroad have fluctuated between $3.5 and $8.2 billion, equivalent to 25% of total remittances for the years 2017 and 2023, as shown in the attached graph. For the year 2023, whose exempt income amounts to $8.2 billion Chilean pesos as already mentioned, they are not only exempt from the tax levied on remittances but are also excluded from the taxable base of the First Category Tax of the Income Tax Law of the companies that pay them. Thus, it is of utmost importance to ensure that the conditions of the exemptions provided by the legislator are met, thus ensuring the corresponding tax compliance.

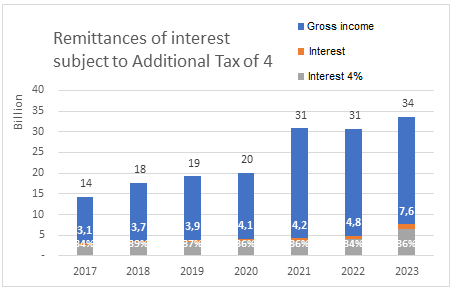

As for remittances associated with interest subject to an additional tax of 4%, the gross income associated with this concept has been increasing over time, with an increase with regard to the transition from the 2020 to 2021 business year. However, interest rates in general and affections at 4% have been maintained over time. Finally, for these last business years, a significant increase can already be seen in terms of interest, going from 4.8 billion CLP to 7.6 billion CLP for the 2023 business year. The above described is shown graphically in the following diagram:

It is worth highlighting the use of information obtained from international organizations

for the construction of the metrics,

which allows for broader monitoring than considering only the controls established

by the Income Tax Law.

Destination countries for cross-border transactions

Regarding the destination countries of cross-border operations, it is observed that remittances abroad, although they were decreasing until 2020, for the year 2021 a slight increase was seen in terms of the countries called "Jurisdiction with Preferential Tax Regime", due to the list that was introduced in article 41 H of the Income Tax Law; a situation that was the same with investments in this type of jurisdiction, since over time these have been decreasing.

About the countries considered as "risk" countries or territories, a list prepared on the basis of information published by international organizations, by virtue of the characteristics of their tax systems, lack of transparency, lack of effective exchange of information and bank secrecy rules, where the destination investments were stable, upward tendencies; however, during the last two tax years these presented a slight drop.

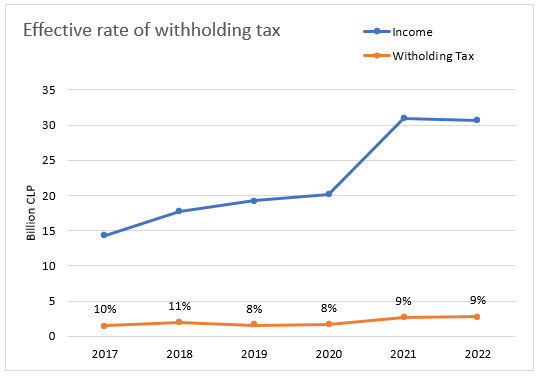

Effective Additional Tax Rates

About the Additional Income Tax, it should be noted that this annual tax affects natural and legal persons who do not have domicile or residence in Chile, applied to the total income received or accrued, in accordance with the concepts and rates defined in the Income Tax Law.The effective rates of additional tax will vary according

to the operation carried out, and we will find ourselves with operations exempt

from this tax, such as certain freight and landing expenses, up to a general

rate of 35% for the total profits remitted abroad or that are withdrawn through

a permanent establishment in Chile.

In turn, whether it is explicit in our legislation, or by the application

of a double tax agreement (DTA), if certain conditions are met, the operation

susceptible to being taxed with additional tax, may be exempt from such tax

or with a reduced rate, as is the case, for example, of interest when they

meet the conditions established in No. 1 of paragraph 4 of Article 59 of the

LIR.

Thus, from the existence of nominal rates for the various operations described

in the Law, because of the application of exemptions or reduced rates, we

can arrive at an effective rate of collection.

As can be seen in the graph below, the effective rates of additional tax have remained between 8% and 9% between the 2019 and 2023 business years, despite the existing increase in total income.

The reduction in the effective rate can be associated with the application of exemptions, or preferential rates, established in our domestic legislation, as well as in the application of agreements to avoid double taxation, matters that are covered in the audit programs established by the International Operations Area, aimed at verifying the correct application of such exemptions or reduced rates.

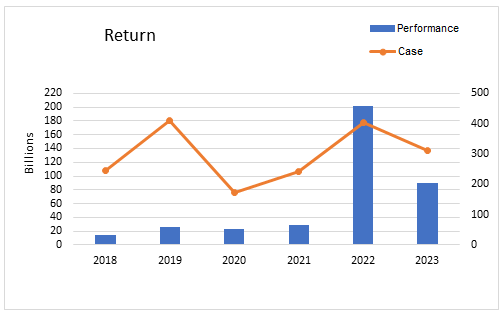

Results of the Strategy for the Compliance of International Operations - Collection

The international strategy has determined a return of 89 billion Chilean pesos of determined tax for the 2023 business year, an amount associated with treatment actions carried out in accordance with the international strategy developed by this Service. This performance is directly linked to the development of 312 cases. It should be noted that the processing actions carried out correspond to both matters of international operations and transfer pricing. This allows the identification of new segments of interest and specific typologies, generating that this is transformed into permanent monitoring.